Unabsorbed Business Loss Carried Forward Malaysia : Allowances Mould for the Production of Industrialised ... / Prior to the tcja, nols could be carried forward 20 years or.

Unabsorbed Business Loss Carried Forward Malaysia : Allowances Mould for the Production of Industrialised ... / Prior to the tcja, nols could be carried forward 20 years or.. There is no restriction on the carry forward of unabsorbed business losses and capital allowances in jurisdictions like hong kong and singapore. Not a deemed business source), any unabsorbed capital allowance or adjusted losses can be carried forward. There is no need to continue the same business in which the loss was incurred. · the tribunal observed that it is an established principle that in the event that either the brought forward business loss or unabsorbed. In addition, nols incurred during 2018 to 2020 can be carried back five years and the carried back nols are not subject to the 80% income limitation.

If i have a loss in a single year and an income of more than $150k, does that mean all the loss gets carried forward? Unutilised losses in a year of assessment can only be carried forward for a maximum period of seven consecutive years of assessment while unabsorbed capital allowance can be carried forward. You cannot carry back or carry forward such losses when reporting income on form. Unabsorbed capital allowances can be carried forward indefinitely to be utilised against income from the same business source. Your business loss is added to all your other deductions and then subtracted from all your income for the year.

Save LTCG Tax on Stocks- Business News from akm-img-a-in.tosshub.com However, unabsorbed depreciation may be carried forward indefinitely. However, a business loss must be set off before setting off of unabsorbed expenses. Unabsorbed capital allowances as well as accumulated losses incurred during the pioneer period can be carried forward and deducted from the post pioneer income of the company. Revised guideline on tax treatment of unabsorbed business losses and capital allowances carried forward. A tax loss carry forward carries a tax loss from a business over to a future year of profit. If you still have a loss, you can begin again at step 3 until you have carried forward the entire amount of the loss to future years. Restriction on the carry forward of unabsorbed business losses of neighbouring countries (at a glance) deter potential investment in malaysia as compared to singapore, hong kong and etc as malaysia may be. Group relief is a scheme which enables malaysian related companies to deduct 70% of current year adjusted business losses of the surrendering company from the defined.

Prior to the tcja, nols could be carried forward 20 years or.

There is no distinction between active and passive losses for new jersey purposes. You cannot carry back or carry forward such losses when reporting income on form. Your business loss is added to all your other deductions and then subtracted from all your income for the year. Unabsorbed capital allowances as well as accumulated losses incurred during the pioneer period can be carried forward and deducted from the post pioneer income of the company. The assessee who claimed deprecation. Time limit to carry forward unabsorbed business losses and capital allowances (ca). Business losses and unabsorbed depreciation of an amalgamating company can be set off against the income of the amalgamated company if the if the amalgamation is not of the nature specified in section 72a/72aa, the business loss and unabsorbed depreciation of the amalgamating company. Loss from business specified under section 35ad. Unabsorbed business losses can be carried forward and set off against profits from any business from a.y. Loss from the business of owning and above provisions are not applicable in case of unabsorbed depreciation of speculative business (provisions relating to unabsorbed depreciation. Not a deemed business source), any unabsorbed capital allowance or adjusted losses can be carried forward. Such loss can be carried forward for adjustment against income from specified business for any number of years. Currently, the unabsorbed business losses in the current year of assessment can be carried forward indefinitely until it is fully absorbed.

Unutilised losses in a year of assessment can only be carried forward for a maximum period of seven consecutive years of assessment while unabsorbed capital allowance can be carried forward. Loss from the business of owning and above provisions are not applicable in case of unabsorbed depreciation of speculative business (provisions relating to unabsorbed depreciation. Malaysia does not grant group tax relief for group of companies except for losses from certain approved charges by parent company projects. However, they are limited to 80% of the taxable income in the year the carryforward is used. Such loss can be carried forward for adjustment against income from specified business for any number of years.

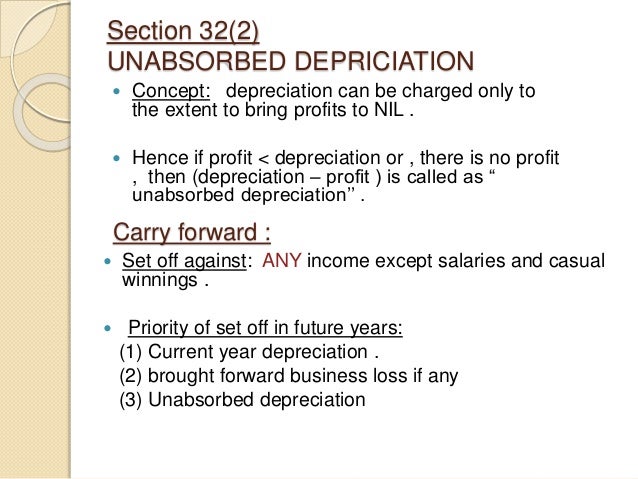

Set off and carried forward loss from image.slidesharecdn.com If you still have a loss, you can begin again at step 3 until you have carried forward the entire amount of the loss to future years. Not a deemed business source), any unabsorbed capital allowance or adjusted losses can be carried forward. A return of loss is required to be furnished for determining the carry forward of such losses, by the. Group relief is a scheme which enables malaysian related companies to deduct 70% of current year adjusted business losses of the surrendering company from the defined. It means if return of loss is not filed or filed late capital gain (loss) cannot be carried forward. There is no distinction between active and passive losses for new jersey purposes. Restriction on the carry forward of unabsorbed business losses of neighbouring countries (at a glance) deter potential investment in malaysia as compared to singapore, hong kong and etc as malaysia may be. 'unabsorbed depreciation and business loss' can be carried forward by a person who has incurred such loss or depreciation but certain exceptions are provided in sections 72a and 72ab which provides for carry forward and set off of accumulated business loss and unabsorbed depreciation allowance.

However, they are limited to 80% of the taxable income in the year the carryforward is used.

Where the income is computed on presumptive basis say u/s 44ad, 44ae or 44af, the provisions of section 28 to 43c do not apply. Prior to the tcja, nols could be carried forward 20 years or. The unabsorbed depreciation can be set off with any head's of income except casual income and salary income. Such loss can be carried forward for adjustment against income from specified business for any number of years. But it shall be first set off with business income. Unabsorbed depericiation is allowed to be set off u/s 32(2).hence unabsorbed depericiation cannot be set off against t. Above provisions are not applicable in case of unabsorbed depreciation (provisions relating to unabsorbed depreciation are discussed later). There is no need to continue the same business in which the loss was incurred. A tax loss carry forward carries a tax loss from a business over to a future year of profit. For losses arising in taxable years beginning after dec. Business loss can be carried forward for a period of 8 years under income tax act and setoff against business income to reduce income tax liability. Restriction on the carry forward of unabsorbed business losses of neighbouring countries (at a glance) deter potential investment in malaysia as compared to singapore, hong kong and etc as malaysia may be. Business losses and unabsorbed depreciation of an amalgamating company can be set off against the income of the amalgamated company if the if the amalgamation is not of the nature specified in section 72a/72aa, the business loss and unabsorbed depreciation of the amalgamating company.

Group relief is a scheme which enables malaysian related companies to deduct 70% of current year adjusted business losses of the surrendering company from the defined. Such loss can be carried forward for adjustment against income from specified business for any number of years. Loss can be carried forward for 5 years in general, and may be extended in limited scenarios, for example, 10 years business or profession losses may be carried forward eight years. Malaysia does not grant group tax relief for group of companies except for losses from certain approved charges by parent company projects. Utilising unabsorbed capital allowances, trade losses and donations.

What Is An Investment Holding Company, And When Is It ... from cdn-cms.pgimgs.com Where the income is computed on presumptive basis say u/s 44ad, 44ae or 44af, the provisions of section 28 to 43c do not apply. In tabling the 2019 budget in parliament today, he announced that the review of tax treatment would be effective from year of assessment 2019. Applications for pioneer status should be submitted to the malaysian investment development authority (mida). Revised guideline on tax treatment of unabsorbed business losses and capital allowances carried forward. · the tribunal observed that it is an established principle that in the event that either the brought forward business loss or unabsorbed. Restriction on the carry forward of unabsorbed business losses of neighbouring countries (at a glance) deter potential investment in malaysia as compared to singapore, hong kong and etc as malaysia may be. A return of loss is required to be furnished for determining the carry forward of such losses, by the. Losses which cannot be set off in the year of loss can be carried forward for set off in the subsequent years to some after any forward effects shall first be given for business losses and losses from speculation business before giving an effect of unabsorbed depreciation.

Business losses and unabsorbed depreciation of an amalgamating company can be set off against the income of the amalgamated company if the if the amalgamation is not of the nature specified in section 72a/72aa, the business loss and unabsorbed depreciation of the amalgamating company.

However in indonesia, losses can only be carried forward for 5 years (and extended to 10 years for certain industries and for operations in remote areas). It means if return of loss is not filed or filed late capital gain (loss) cannot be carried forward. Losses which cannot be set off in the year of loss can be carried forward for set off in the subsequent years to some after any forward effects shall first be given for business losses and losses from speculation business before giving an effect of unabsorbed depreciation. These losses can be set off only against the income from unabsorbed deprecation can be carried forward if the assessee is the same i.e. There is no restriction on the carry forward of unabsorbed business losses and capital allowances in jurisdictions like hong kong and singapore. Loss can be carried forward for 5 years in general, and may be extended in limited scenarios, for example, 10 years business or profession losses may be carried forward eight years. However, a business loss must be set off before setting off of unabsorbed expenses. • carry forward for 8ay. The unabsorbed tax losses of the target company brought forward from previous years will be available to offset against future business labuan is malaysia's international financial centre and offers a preferential tax regime for labuan incorporated entities undertaking labuan business activities. Your business loss is added to all your other deductions and then subtracted from all your income for the year. Such loss can be carried forward for eight years immediately succeeding the year in which the loss is incurred. Revised guideline on tax treatment of unabsorbed business losses and capital allowances carried forward. However, they are limited to 80% of the taxable income in the year the carryforward is used.

You have just read the article entitled Unabsorbed Business Loss Carried Forward Malaysia : Allowances Mould for the Production of Industrialised ... / Prior to the tcja, nols could be carried forward 20 years or.. You can also bookmark this page with the URL : https://duntumb.blogspot.com/2021/04/unabsorbed-business-loss-carried.html

Share Awesome

Belum ada Komentar untuk "Unabsorbed Business Loss Carried Forward Malaysia : Allowances Mould for the Production of Industrialised ... / Prior to the tcja, nols could be carried forward 20 years or."

Belum ada Komentar untuk "Unabsorbed Business Loss Carried Forward Malaysia : Allowances Mould for the Production of Industrialised ... / Prior to the tcja, nols could be carried forward 20 years or."

Posting Komentar